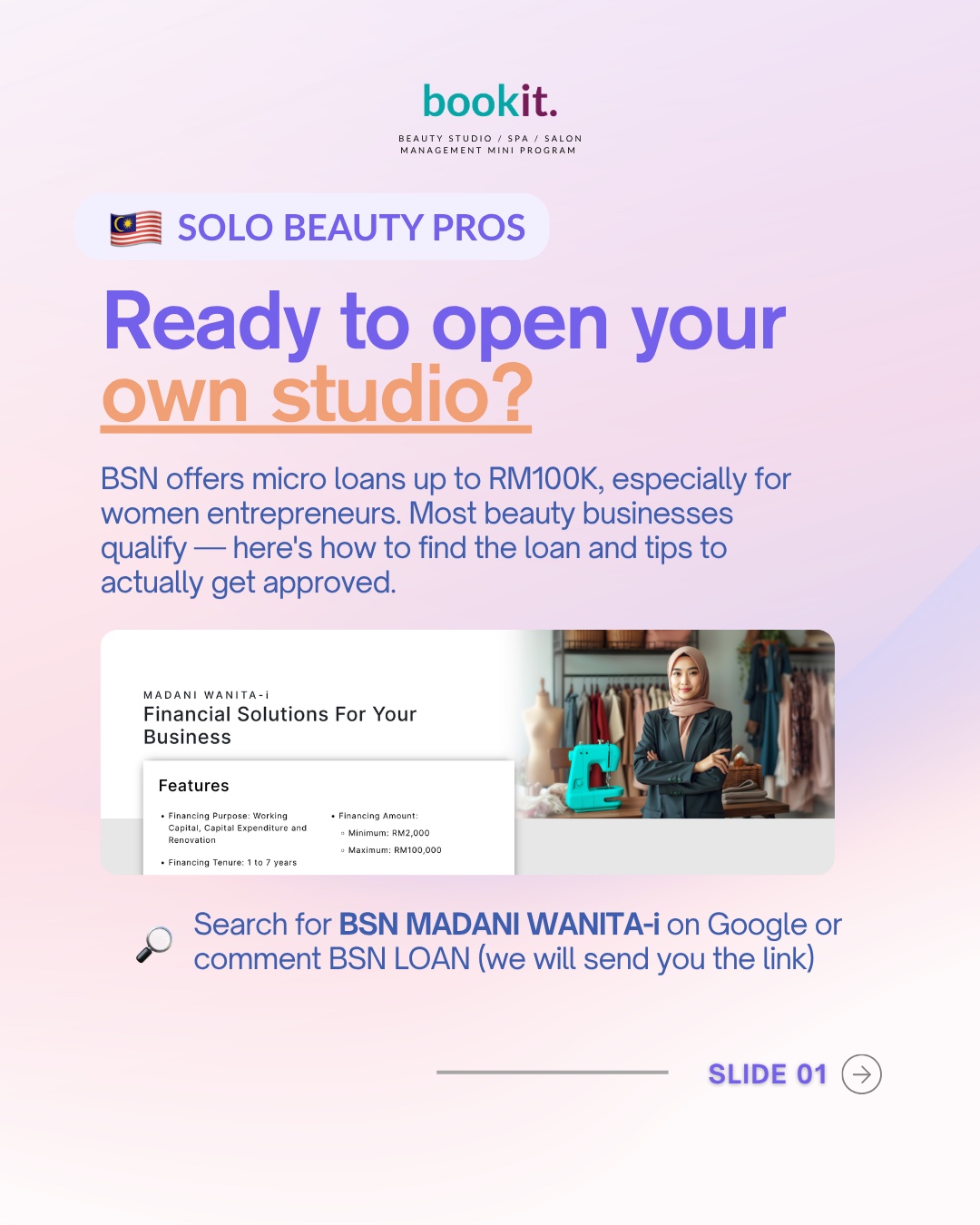

If you've been thinking about opening your own beauty studio — or growing the one you already run — there's a financing option most Malaysian women business owners don't know about: BSN MADANI WANITA-i.

It's a Bank Simpanan Nasional (BSN) micro-financing programme specifically for women entrepreneurs. You can borrow from RM2,000 up to RM100,000, with a tenure of 1 to 7 years. It's Shariah-compliant, and it's designed to support working capital, capital expenditure, and business renovation.

Translation: salons, lash studios, nail bars, spas, brow studios, hair salons — almost every kind of beauty business already qualifies on the business-type criteria. What stops most owners from getting approved isn't eligibility. It's preparation.

We sat down with merchants who got approved (and a few who got rejected) to figure out what actually makes the difference. Here's what we learned.

Where to find the loan

Two ways. You can Google "BSN MADANI WANITA-i" — the official BSN product page comes up first, with the application form and full T&Cs. Or you can walk into any BSN branch and ask for the MADANI WANITA-i micro-financing form. Bring your IC and SSM registration.

Key product details to know before you walk in:

| Item | Detail |

|---|---|

| Financing amount | RM2,000 – RM100,000 |

| Tenure | 1 to 7 years |

| Purpose | Working capital, capex, business renovation |

| Eligibility | Malaysian women entrepreneurs |

| Type | Shariah-compliant (Islamic financing) |

The official terms can change — always confirm on the BSN site before applying.

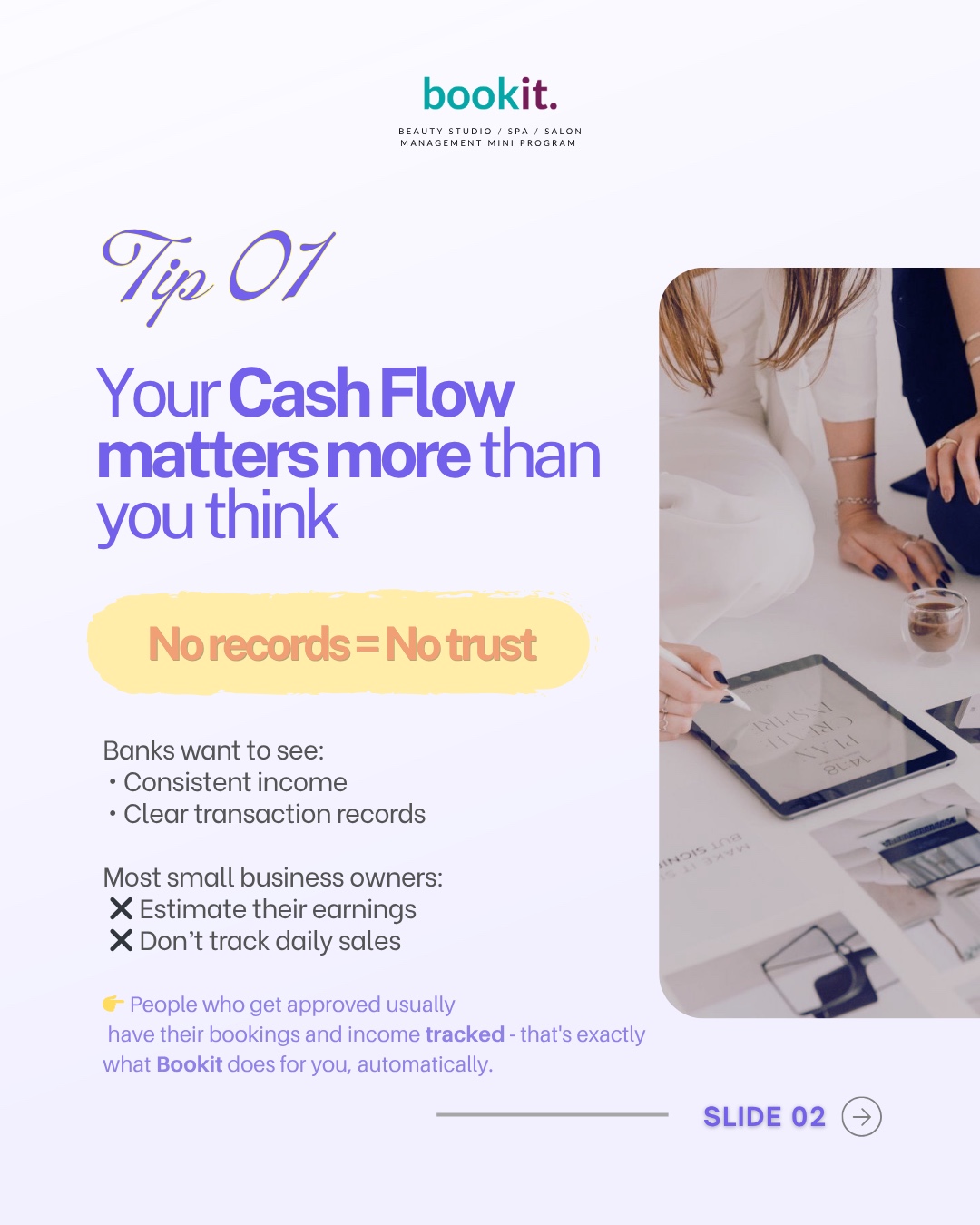

Your cash flow matters more than you think

The single biggest reason beauty businesses get rejected isn't because the business is bad. It's because there's no proof the business is real.

When a bank looks at your application, they're answering one question: can this person pay us back every month? The only way they can answer that is by looking at evidence of money coming in. Not your Instagram followers. Not your booking screenshots. Bank-quality records — consistent income, clear transactions, a paper trail.

What banks want to see is straightforward: consistent monthly income (even a modest amount, as long as it's stable), clear transaction records (receipts, invoices, payment history), and a clean separation between business and personal money. What most small business owners actually do is the opposite: they estimate their monthly earnings ("I think I make about RM6k a month?"), they don't track daily sales because money goes straight from customer to phone wallet to dinner, and they mix everything in one personal bank account.

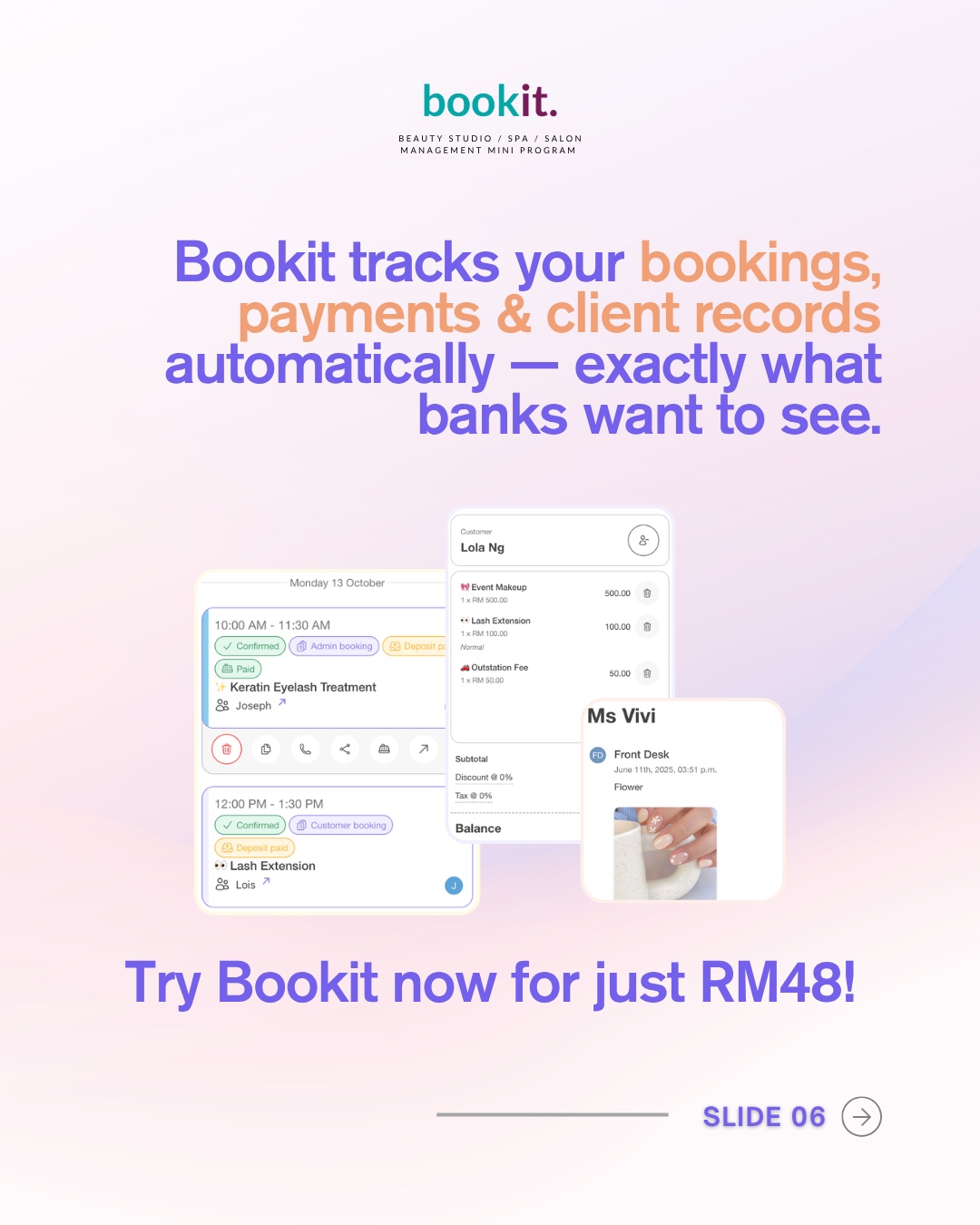

If your cash flow lives in your head instead of in records, the bank has no way to evaluate it. People who get approved usually have their bookings and income tracked — that's where having a proper system (a booking app, POS, accounting tool, or even a disciplined spreadsheet) starts paying for itself long before the loan comes through.

Reality check: 3 months of clean, exportable transaction records will outperform 3 years of "I swear I make RM10k a month" every time.

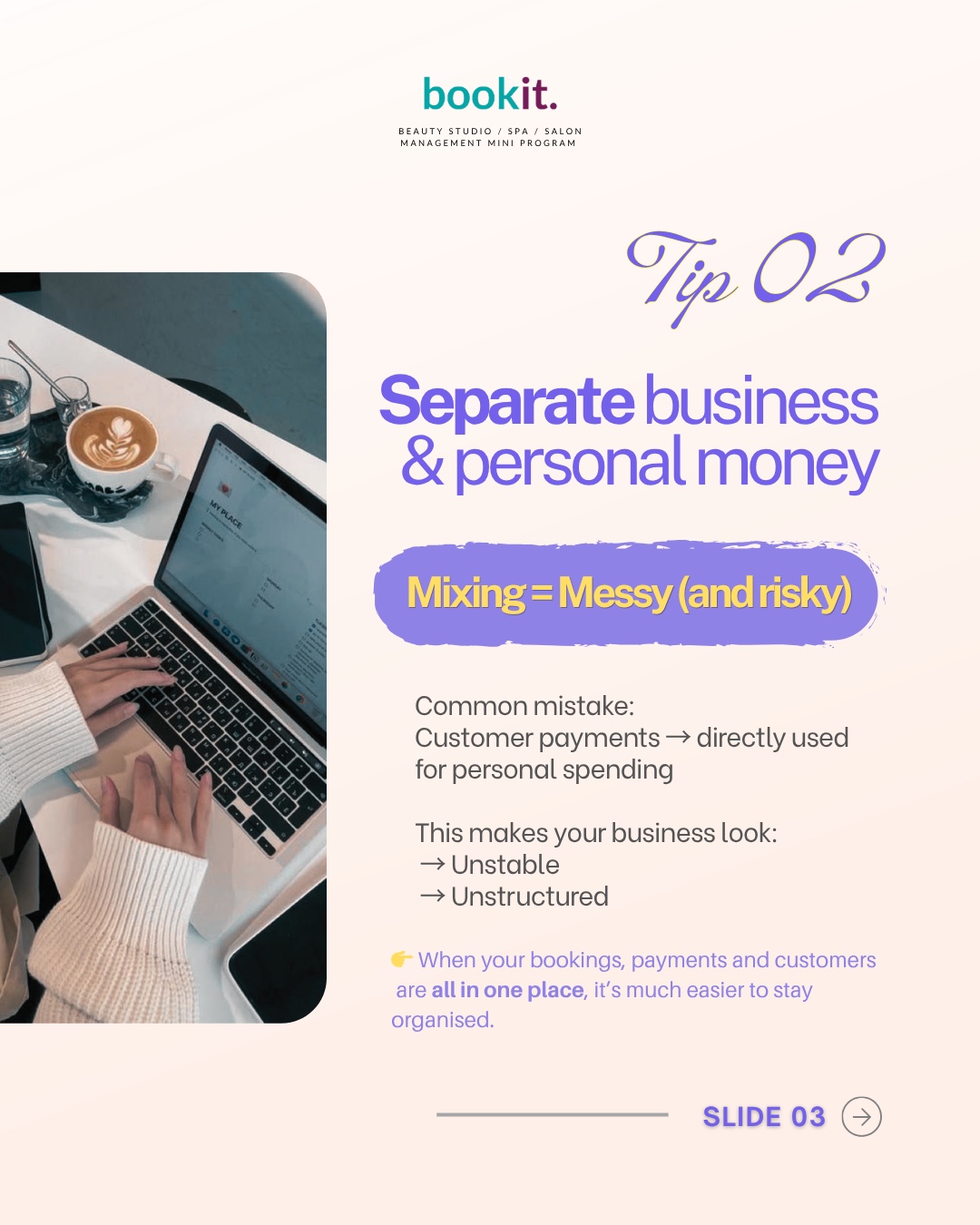

Separate business and personal money

This is the second silent killer. A customer pays you RM250 for a lash treatment. You transfer half to your kid's school account, take RM50 cash, and the rest sits in your personal e-wallet for groceries. By next week, there's no way to tell that RM250 was ever revenue.

When a banker pulls your statement, they don't see a beauty business. They see a personal account with money coming in and out in random amounts. This makes your business look unstable (banks can't see the consistent income pattern they need) and unstructured (no separation between business and personal finances suggests no business discipline).

The fix is simpler than people think. Open a separate bank account for the business — many Malaysian banks let you open a small-business or sole-proprietorship account with just your SSM certificate. All customer payments go in there. Every QR code, every bank transfer, every cash deposit. Then pay yourself a fixed amount each month from the business account to your personal account. That's your "salary".

The moment you do this, three things happen at once: your business looks 10× more professional, your tax filing becomes simpler, and your loan application has a clean, dedicated statement to point to. If your bookings, payments, and customer records all sit in one place (a salon app, a POS system, or both), the separation gets even cleaner — you can export a single statement that shows exactly what came in, when, and for what service.

Show that your business has demand

This is the one most beauty entrepreneurs get backwards. They show up to the bank with a folder full of Instagram screenshots — look, 12k followers! — and assume that's proof of demand.

It isn't. Followers ≠ paying customers. Banks have learned this lesson many times over.

What banks actually look for to gauge demand: repeat customers (people coming back means people are happy paying), consistent booking volume (bookings spread across weeks and months, not just a viral spike), and a real customer list (names, contact, what services they took, when). What is not proof of demand: Instagram follower count, TikTok views, or likes on your last reel.

A simple booking history can say more than your follower count ever will. If you can hand over a printout that shows "Lola Ng — 4 lash refills between Jan and May 2026, average spend RM180", you've made the bank's job easy. They don't need to imagine your business — they can see it. This is exactly the kind of record bookit (and similar tools) build for you automatically as you work. You don't need to do anything special to "prepare" the data — it's already there.

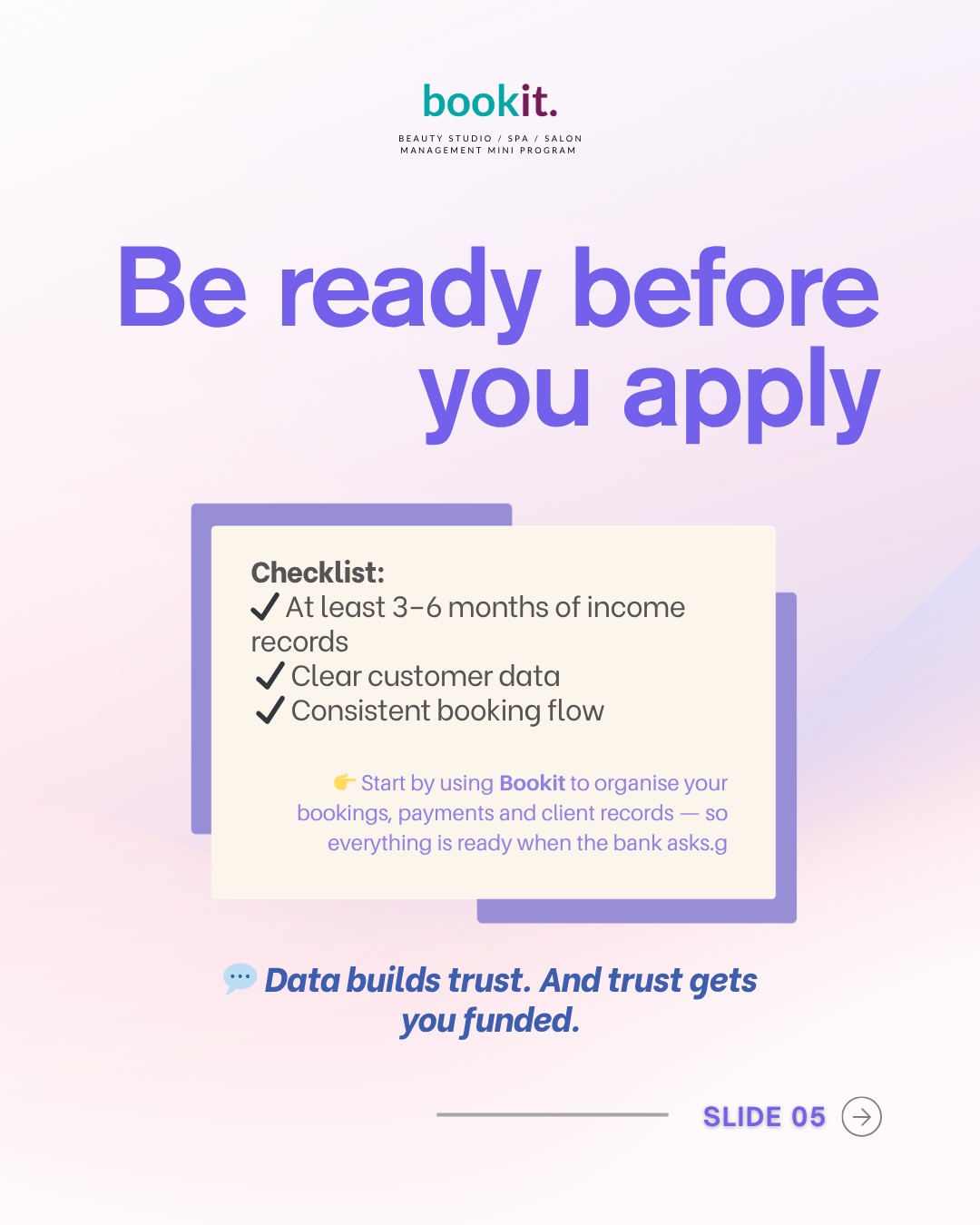

The pre-application checklist

Before you walk into BSN, have these ready:

- ✅ At least 3–6 months of income records — bank statements showing customer payments coming in

- ✅ Clear customer data — a list of clients, services, and dates (this is your CRM)

- ✅ Consistent booking flow — proof that bookings come in regularly, not just from one influencer mention

- ✅ SSM business registration (if you don't have one yet, get it — it's RM30–RM60 and takes a day)

- ✅ Your IC and a copy

- ✅ Latest 3 months of bank statements (business account if you have one, personal if not — but separated as much as possible)

Optional but powerful: a one-page summary of your business (what you do, who your customers are, average ticket size, monthly revenue, how the loan will be used), photos of your current setup, and a simple sentence about how this loan will help you grow. ("Adding a second treatment bed to handle weekend overflow" beats "for the business" every time.)

Data builds trust. And trust gets you funded.

How long does the process take?

From the merchants we've spoken to: expect 2–4 weeks between application and approval if everything is in order, longer if BSN comes back asking for more documents.

The single biggest delay is almost always incomplete records — the bank asks for proof of income, you have to dig through 6 months of WhatsApp messages and bank transfers, and the process stalls. Owners who already have a clean POS or booking system in place tend to close the loop in days, not weeks.

Common reasons applications get rejected (or delayed)

Five things, in rough order of how often we see them. Estimated income only (no actual records to back it up). Mixed personal/business account with no way to separate transactions. Business is too new — most lenders want to see at least 3 months of operating history, some want 6. Inconsistent transactions — three big deposits in March, nothing in April, two small ones in May reads as "unpredictable" to a banker. And no SSM registration (this one is fixable in a day — just do it).

None of these are about your business being bad. They're about your records being thin.

What to do next

This is the part where we'll be direct: this is exactly what we built bookit to do. As you book customers, take payments, and finish appointments, bookit is silently building the records the bank wants to see — consistent income, clear transactions, a real customer list with service history. When you apply for the loan, you can export a single statement that shows everything: monthly revenue, transaction-by-transaction breakdown, customer list, booking volume by month. The kind of document a banker can read in 30 seconds and say "yes, this is a real business."

You don't have to use bookit, of course — any system that produces clean, exportable records will do the same job. The point is: have a system. Don't let your business live in your head when you need to prove it to someone who's never met you.

If you want to give bookit a try, the RM48 trial gets you the full app for a month. That's enough time to capture your next batch of bookings cleanly and have something real to bring to the bank.

Heads-up: BSN's product details (rates, tenure, eligibility) can change. Always check the latest terms on the BSN website before applying. This article is general guidance, not financial advice.