If you run a beauty studio in Malaysia and you've ever watched a client almost book a premium package — and then back out at checkout because of the upfront cost — this is for you.

Buy Now Pay Later (BNPL) is the simplest way to fix that. It lets your clients split a treatment into smaller instalments — zero interest, zero hassle on their side — while you still get paid in full, upfront. The BNPL provider takes the risk; you take the booking.

In the Malaysian beauty market right now, BNPL isn't a luxury feature. It's becoming the difference between a client who books the RM600 package and a client who walks out. Here's the full playbook.

How your client actually experiences BNPL

From the client's side, it's invisible until checkout. The flow is simple: they book a treatment, they choose PayLater at checkout (same as picking GrabPay or FPX), the payment gets split into instalments by the BNPL provider, and they enjoy the treatment immediately — no waiting, no escrow.

The mental shift this creates is huge. Compare "RM600 upfront" to "RM200 × 3 months." It's the same money in the end, but the payment pressure is what kills conversions on premium services. Most clients pause at RM600, mentally check their account balance, think about rent, and either delay the booking or pick a cheaper service. The same client framed with RM200 × 3 months says yes far more often — it slots into their head alongside Spotify and Netflix, not as a separate financial event.

Industry-wide, merchants who offer BNPL typically see average order value rise 30–60% for treatments above RM300, and cart-abandonment drop at checkout. For Malaysian beauty studios, this often means the RM800 lash bonding upgrade or the RM1,500 6-session package goes from "let me think about it" to "let's book it now."

Lower payment pressure = higher chance of conversion.

The four main BNPL options for Malaysian merchants

There's no single "best" BNPL — each has a slightly different user base. As a Malaysian beauty merchant, you typically want to support the one or two your actual clients already use.

SPayLater (Shopee) is available via ShopeePay, with installment options up to a few months. It's popular among younger users — Gen Z, university students, and anyone who already shops on Shopee weekly. Best fit for nail studios, lash bars, and brow studios with a younger client base.

GrabPayLater is available via the Grab app. Flexible payment options, and especially convenient for daily Grab users — anyone who uses Grab for food, rides, or groceries already has access without needing to install anything new. Best fit for urban salons in KL, PJ, or Penang where most clients are already Grab regulars.

Atome PayLater is available via the Atome app and splits payments into monthly instalments, typically over 3 months. Atome is most heavily used in fashion and beauty spending specifically, so it slots naturally into a beauty studio's checkout. Best fit for spas, premium salons, and anywhere the average ticket is RM300+.

Split (by Visa) is available via Visa-supported banks. Unlike the others, it converts existing card purchases into installment plans after the fact — so there's no separate app for clients to install. Best fit for salons whose clients tend to pay by card already.

You don't need all four. Two is usually plenty. The pragmatic shortcut: ask your last 20 clients what payment apps they use (just look at how they're paying you now), pick the top one or two, and call that your BNPL stack. For most Malaysian beauty studios, the answer ends up being SPayLater + one of Atome/Grab.

What happens on your side as the merchant

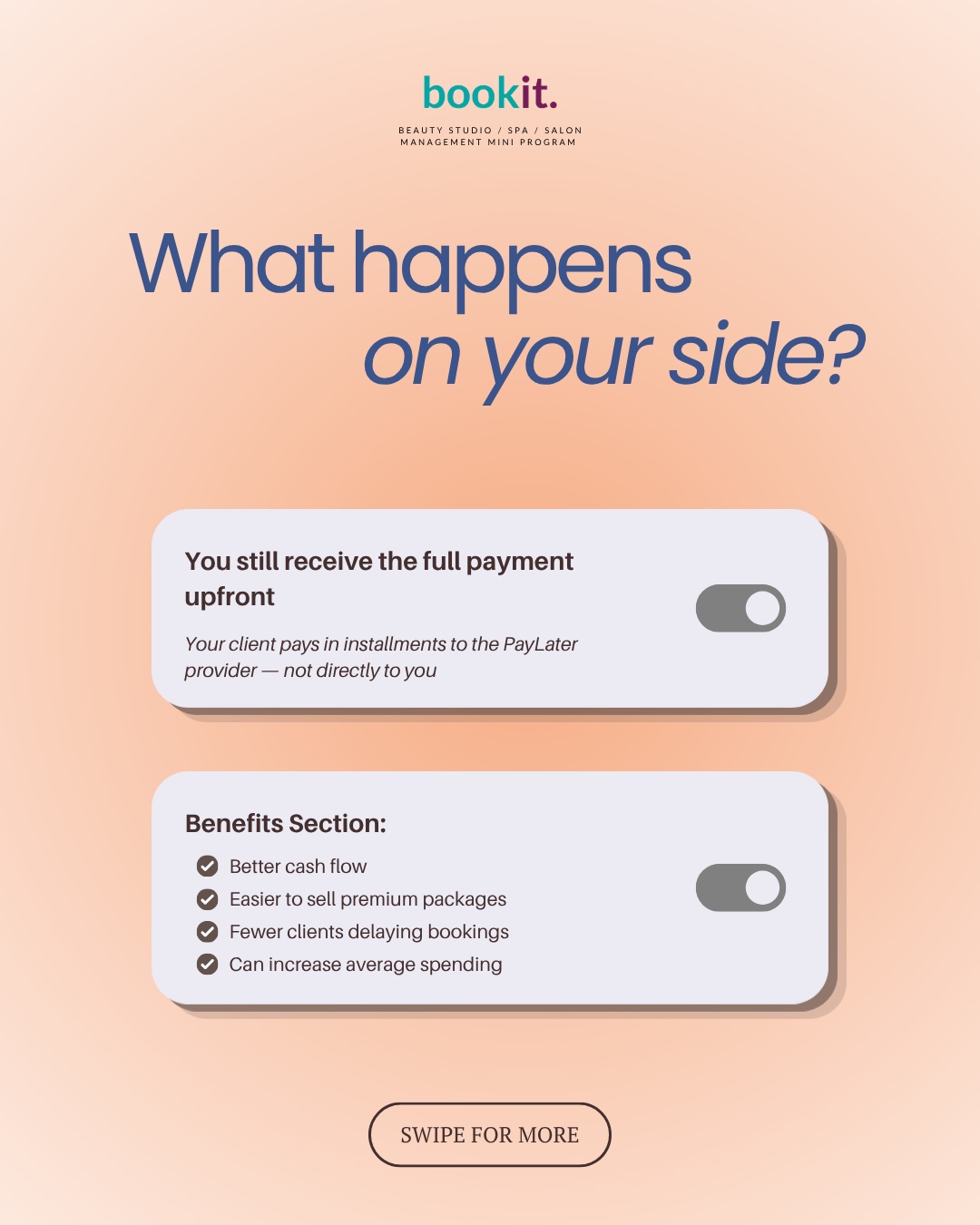

This is the part most beauty owners get wrong about BNPL — they assume they are giving the loan to the client. They're not.

You still receive the full payment upfront. The client pays in instalments to the BNPL provider — not directly to you. The provider takes on the default risk, the collection, and the relationship with the client's bank. Your relationship is just: client walks in, picks BNPL at checkout, you get paid the full amount within 1–3 business days, depending on the provider.

The benefits stack up quickly. Better cash flow — you get the lump sum upfront while the client spreads their cost. Easier to sell premium packages — the RM2,000 6-session package no longer feels out of reach. Fewer clients delaying bookings to wait for payday. Higher average spend per client, because when payment friction drops, ticket size goes up. The merchant fee is real (we'll cover that below), but for any service above ~RM300, the lift in conversion and ticket size typically more than covers it.

How to apply as a merchant

Each provider's process is slightly different, but the broad steps are the same. Plan for 3–7 working days end-to-end.

You start by registering online at the provider's merchant portal — merchant.shopee.com.my, merchant.grab.com, merchant.atome.my, or your bank's Split portal — and filling in your details. Then you submit your documents: SSM registration, IC copy, and business bank account info. Approval usually comes back in 3–7 working days; beauty businesses with a clean SSM and a year-plus of operating history get approved fastest. Once approved, you get a QR code or payment link, which you can display at your studio or share directly in WhatsApp. Then it's time to start accepting — but don't just enable it. Promote it. We'll get to that in the last section.

The single biggest cause of "your application is still pending" is inconsistent or missing business documentation — typically an SSM number that doesn't match the bank account name, or no clean business bank account at all. Fix those before you apply and most providers will approve in days, not weeks.

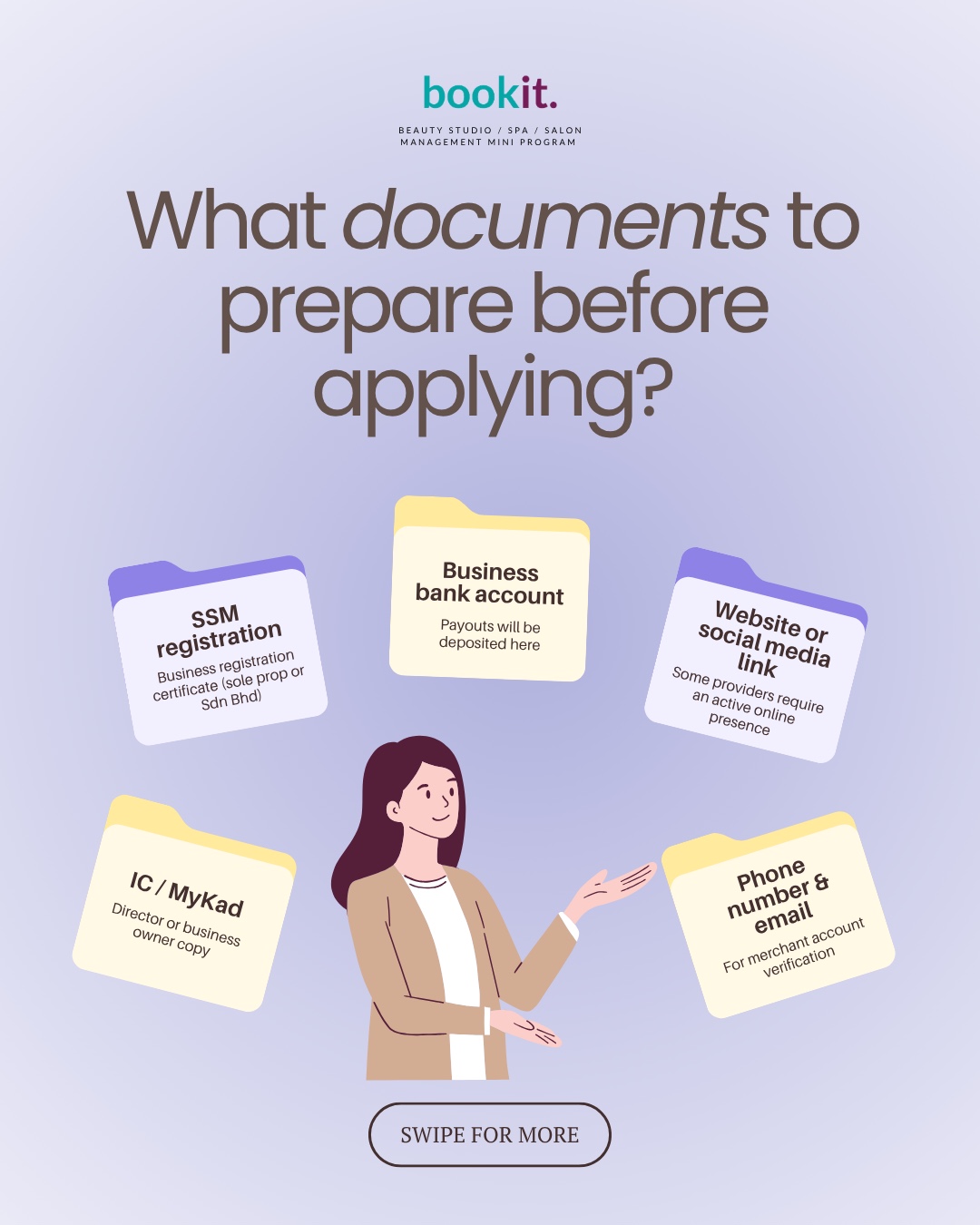

What documents to prepare before applying

Get these ready before you start the application — it's the difference between a 3-day approval and a 3-week back-and-forth.

| Document | What it's for |

|---|---|

| SSM registration | Business registration certificate (sole prop or Sdn Bhd) |

| Business bank account | Where the BNPL provider will deposit your payouts |

| IC / MyKad | Director's or business owner's copy |

| Website or social media link | Some providers require an active online presence |

| Phone number & email | For merchant account verification |

Optional but useful: a short business description (what you do, average ticket size, monthly revenue), photos of your physical location (helps with verification for brick-and-mortar businesses), and 3 months of bank statements (some providers ask, some don't).

If you've already followed our guide to getting business records loan-ready, you have most of this organised. The same documents work for both BNPL and a BSN micro loan — set them up once, use them for everything.

Is BNPL right for your beauty business?

It's not a fit for every business. Here's the honest call.

Why it works: it increases average spend per client, makes premium services easier to book, you still receive full payment upfront, it gives your salon a competitive edge (most salons in Malaysia still don't offer this, so you'd stand out), and setup is simple with no technical skills required.

Things to note: merchant fees usually range from ~1.5–5% per transaction depending on provider and category. Not all clients will be eligible — they need to qualify with the provider, so think of it as an "opt-in upgrade" not a universal payment method. Default risk is handled by the BNPL provider, but the provider may decline applications, especially for higher-value purchases. Payout timing differs by provider — anywhere from same-day to T+3 working days.

The rough rule of thumb: if your average ticket is below RM150, BNPL is overkill — the fees eat the margin and clients don't really need to split RM80 anyway. If your average ticket is RM300+, or you sell packages of RM800+, BNPL almost always pays for itself within 1–2 months of enabling it.

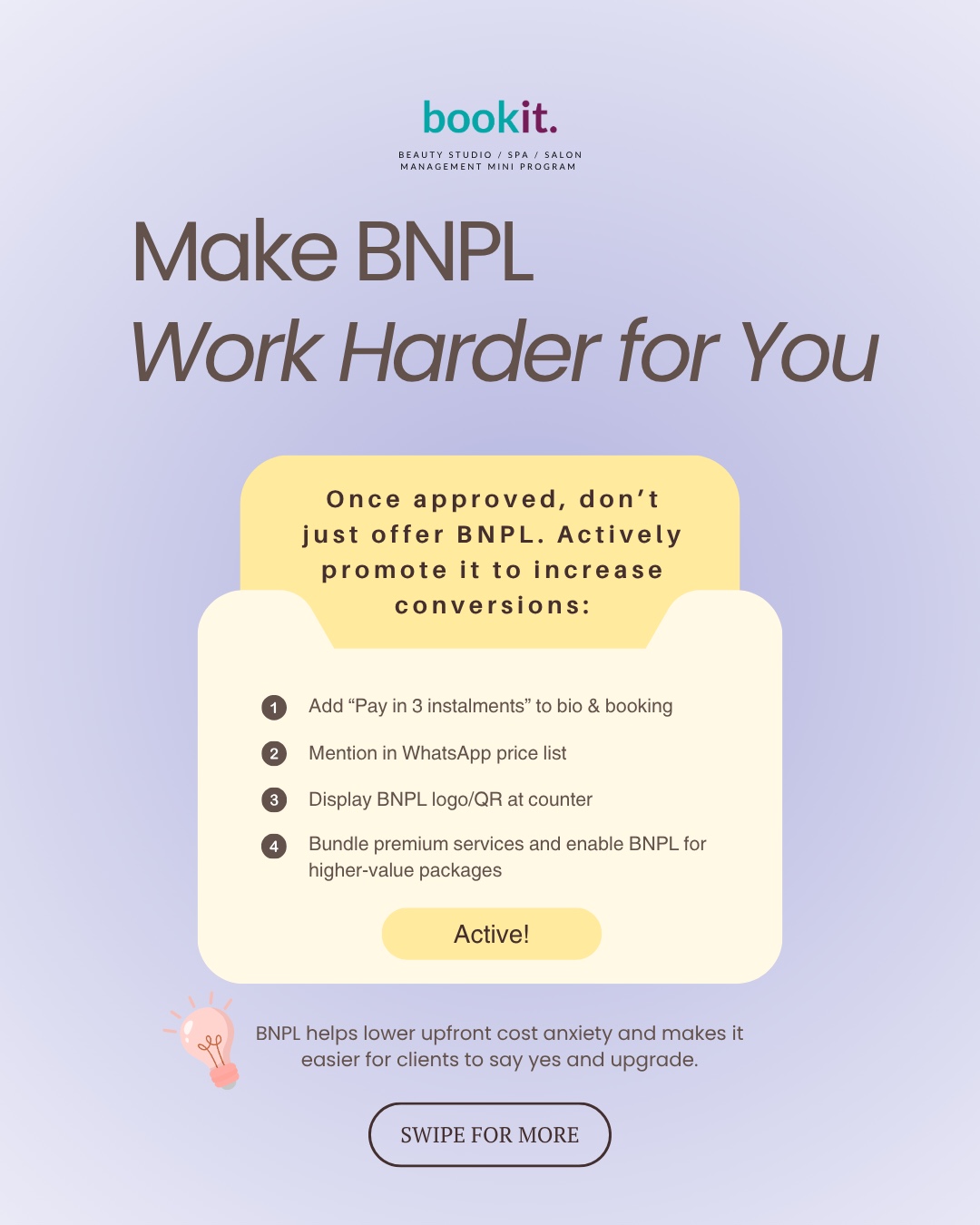

Make BNPL work harder for you

This is the step most merchants skip — and the reason BNPL "doesn't seem to work" for them. Just enabling BNPL is not enough. Most clients don't know it's an option unless you tell them. Once you're approved, promote it.

There are four things to do in your first week. First, add "Pay in 3 instalments" to your bio and booking link. Your Instagram bio and your booking page should both say this clearly — "Pay in 3 with Atome 💜" on the booking page can lift conversion by 20%+ on premium services. Second, mention it in your WhatsApp price list. When you send a client your menu, drop the line: "Pssst — we accept SPayLater & Atome for 3-month split if needed 🥰". Third, display BNPL logos and QR codes at the counter. Physical signage matters. A small acrylic stand with the SPayLater and Atome logos turns "how much again?" into "oh, can I split?" Fourth, bundle premium services and enable BNPL on them specifically. Create an RM1,500 6-session package and explicitly market it as "RM250/month with BNPL". The same package without that framing converts at half the rate.

BNPL helps lower upfront cost anxiety and makes it easier for clients to say yes and upgrade.

What to do next

Offering BNPL is one piece of a bigger picture: making payment frictionless. The salons we work with who lift their average ticket the fastest tend to have all of these in place at once — a booking link so clients self-serve, deposits at booking to lock in commitment, BNPL at checkout to remove upfront-cost anxiety, and stored client preferences so they feel known and rebook faster. Each one alone is a small lift. Stacked together, it's a different business — and crucially, less of your time spent chasing payments and confirmations.

If you'd like to see what that looks like end-to-end (including BNPL integration alongside e-wallets, FPX, and cards), the bookit RM48 trial gives you the full app for a month. We can walk you through enabling BNPL on your bookings personally — most merchants get their first BNPL booking within the first week.

Heads-up: BNPL provider terms (fees, eligibility, payout timing) change regularly. Always confirm the current rates on each provider's merchant portal before applying. This article is general guidance, not financial advice.